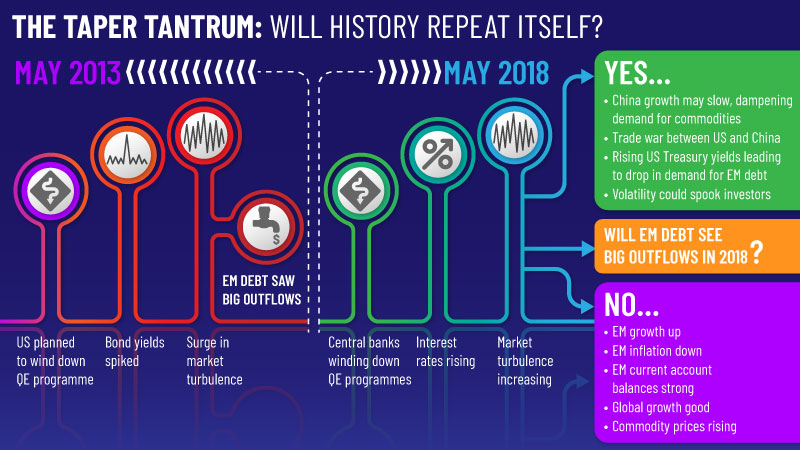

In May 2013, the US Federal Reserve announced it planned to wind down its bond-buying programme. In the ensuing financial turbulence bond yields spiked, emerging markets took a hammering and the ‘taper tantrum’ entered markets folklore.

Five years on, as central banks phase out quantitative easing and tighten monetary policy, it is reasonable to assume that emerging markets will get hit by similarly capricious capital outflows.

Investor interest in the developing world has been sky high. Foreign investment in emerging markets jumped 54% last year to €191bn (£167bn, $226bn) and the lion’s share (€138bn) was in emerging markets debt, according to the Institute of International Finance.

“Emerging market fundamentals are more robust than they’ve been for years.”

“The stars were in near-perfect alignment for emerging market debt investors in 2017,” says Colm McDonagh, head of emerging market fixed income at Insight Investment.

“Sovereign and corporate spreads tightened by 57 basis points and 43bp respectively, and local currency yields ended 65bp lower.”

But as US Treasury yields rise and market volatility increases, will these robust foreign inflows continue?

The Fed raised its benchmark interest rate by a quarter of a percentage point in March – the sixth hike since near-zero levels in 2015 – and new Fed chairman Jay Powell suggested the pace of future hikes could be more aggressive amid positive economic tailwinds.

The market expects a further three or four rate rises this year.

Improved fundamentals

In the past, such a sharp increase in the cost of borrowing would have spelt trouble for the developing world (take, for example, the Mexican debt crisis in the mid-’90s when a Fed rate hike left the country unable to service its dollar-denominated debts.)

However, Liam Spillane, head of emerging market debt at Aviva Investors, says the impact of rising rates on emerging markets is not the harbinger of doom it once was.

“Emerging market fundamentals are more robust than they’ve been for years,” he says.

Emerging markets on JP Morgan’s GBI-EM index have generally seen a pickup in growth, a decline in inflation and improved current account balances in recent years.

Currency valuations are fair and monetary policy measured. Corporates generally have strong balance sheets – as evidenced by low leverage levels and high cash balances – and default rates on emerging market credit are at record lows.

Part of the reason for emerging markets’ robust performance over the past year has been the synchronised global growth outlook.

The IMF forecasts global growth of 3.9% this year and next – up 0.2% on 2017.

“Emerging markets have benefited from a favourable economic backdrop characterised by good economic growth momentum, healthy inflation dynamics and solid exports,” says Gergely Majoros, a member of investment committee at Carmignac.

“The positive growth outlook and favourable US financial conditions are expected to further support capital flows into emerging markets assets.”

The weak dollar – which has fallen more than 13% against the euro since the start of 2017 – has helped stabilise commodity prices, which has boosted emerging economies.

Commodity prices have risen 30-40% on average from the lows of 2015.

The political situation, meanwhile, is improving in many countries. Indian prime minister Narendra Modi’s pro-business reforms and new South African president Cyril Ramaphosa’s anti-corruption agenda should boost investment opportunities.

“Structural reforms in commodity producing countries have contributed to significantly improved current account balances,” says Majoros.